BRRRR (BUY, REHAB, RENT, REFINANCE, AND REPEAT)

This is Blog Post 6 of The Getting Started in Real Estate Series. Today’s topic is the BRRRR strategy.

BRRRR is one of the favorite real estate investing strategies among the real estate investing community and you will see why below.

So, what is BRRRR?

The basics:

- You Buy a property that needs work

- Renovate it (just enough).

- By doing this, you end up increasing the value of the property. This is also known as forced appreciation.

- Rent it at market rent

- Go to a bank, get a cash-out Refinance loan.

- Because you increased the value of the property by doing the right type of renovation, the bank gives you a loan that will cover either 100% of what you spent or close to that.

- Once you get your money back, you Repeat the process and do it all over again.

In a perfect BRRRR 🥶 , you would get 100% of your money back while still cash flowing. I call this BRRRRfection.

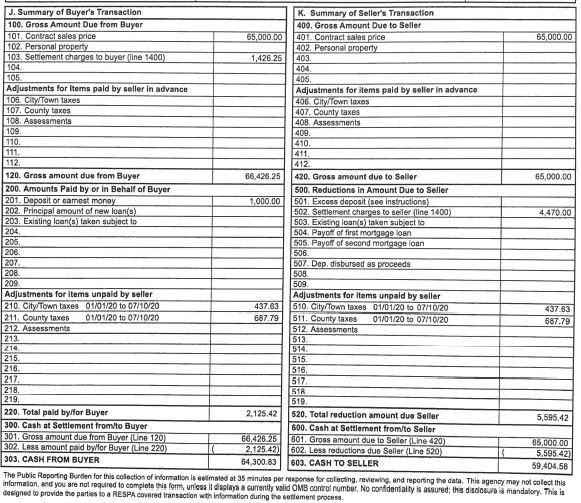

We have done a few BRRRR deals, but I can’t say that I’ve accomplished BRRRRfection yet. At least, not by the book definition. However, the few we’ve done still fall under the BRRRR category. I’ll walk you through a real example. I had to dig out the actual numbers

BRRRR Example – The Big Horn Property

The Facts

| Cash at Purchase | $65,300 |

| Renovation Costs | $22,811 |

| Holding Costs (insurance, utilities, interest, etc) | $1,498 |

| Total Cost | $89,609 |

| Appraised Value after rehab | $130,000 |

Scenario A: The traditional BRRRR strategy would have looked like:

| Refinance Loan at 75% of Appraised Value of $130,000 | $97,500 |

| Minus Closing Costs | ($5,208) |

| Minus Total Cost of Property + Rehab | ($89,609) |

| Total Net Cash Out from Refinance | $2,683 |

In the scenario above, I would have recouped all of my money and be left with an extra $2,683, but I didn’t do this because I had a different strategy in mind. I wanted to leave this property with a higher cash flow while using the remainder equity to get a HELOC (Home Equity Line Of Credit).

Scenario B: The Refi/HELOC BRRRR strategy

| Refinance Loan to Cover Purchase Price only (50% of Appraised Value) | $66,000 |

| Minus Loan Costs | ($5,208) |

| Minus Total Cost of Property + Rehab | ($89,609) |

| Total Net Cash Left in the Deal | ($28,817) |

We left a significant amount of money in the deal, but for a good reason. We wanted higher monthly cashflow and the opportunity to pull out equity by using an equity line of credit. We wanted to have more borrowing options for buying future deals without having to be locked to a fixed mortgage interest payment. We would use the line for temporary funding and pay it down as we refinanced properties.

I also wanted to mention that in Scenario A, I would have had to wait an additional 2 months to be able to get a loan for the $97,500 which in turn would have resulted in additional holding costs. Most lenders have a 6-month “seasoning” period before letting you take out a mortgage that is higher than purchase price and closing costs. In our case, we were capped at $66,000 which was purchase price of $65,000 plus closing costs of $1,000. You can always find a lender that will waive the “seasoning” requirement, but don’t be surprised if you bump into this.

Two months after we closed on the mortgage, we applied through a credit union and got approved for a $38,000 line of credit which we then used to fund another deal. At the end, we ended up getting $104,000 out this property. If I had done the traditional BRRRR strategy, the max I would have gotten was $97,500 so it’s still a winner.

How Secured Line of Credits or (HELOC) work :

- You have a property that is appraised at $130,000 and a mortgage of $66,000. A lender may give you a 80% loan to value secured credit line. What this means is that the bank will give you a line of up to $104,000 (80% of $130k) minus the mortgage. This would be $38,000 ($104k-$66k) which is what we got.

- A secured line of credit means that if you default, they can try to foreclose in the property.

- A secured line of credit is like a credit card in that it revolves, except that you can take large amounts of cash out and pay only 4% interest.

- You draw money when needed and repay as you go. We used the $38,000 line to buy another property cash.

- With this strategy, you are playing the long game. Now you have more funding to buy more if this is something you would like.

Let’s talk Cash Flow

One of the BRRRR pitfalls is that pulling too much equity can result in negative or very low monthly cash flow. The mortgage payment may end up eating all of your revenue. Yes, you may end up with infinite return because you didn’t put any money down, but do you really want a property that doesn’t cash flow. Let me compare the cash flow from scenario A vs B above.

| Rent | $1,200 | |

| Minus: Vacancy Reserve 10% | ($120) | |

| Minus: Property Management 10% | ($120) | |

| Minus: Maintenance Reserve 10% | ($120) | |

| Minus: Capital Expenditures 5% | ($60) | |

| Minus: Insurance | ($55) | |

| Minus: Property Taxes | ($150) | |

| Net Operating Income (Income before debt payments) | $575 |

Next, let’s see how much cash flow we get from each scenario above. Scenario A is the $97,500 mortgage and scenario B is the $66,000 mortgage.

| Mortgage Service | Scenario A $97.5k | Scenario B $66k |

| Net Operating Income | $575 | $575 |

| Monthly Mortgage Interest & Principal @ 3.99% interest | ($465) | ($317) |

| Net Cash Flow | $110 | $258 |

As you can see above, either scenario would have been okay. It’s just a matter of choosing the best path for YOUR specific long-term goals.

Let’s Recap

If done right, BRRRR is a great way to get started in real estate without money. We discussed two approaches:

- You can take all of your cash out if the property allows it.

- Leave money in the deal temporarily and then get a secured line of credit.

Pros:

- Potential to higher return

- You force appreciation of the property and build equity

- You may potentially get all of your money back

- With a combination of loans, you may be able to buy without any of your own money

- Getting cashback from refinancing is not a taxable event. No taxable gains until sold.

You may end up taking out too much cash and be left with no cash flow

Cons:

- Similar to a Flip, you are counting that the value of the property will be valued at an amount higher than the purchase price and the cost of repair.

- The risk is that you may overdo it with the renovations or over estimate the after repair value (ARV).

- You may end up taking out too much cash and be left with no cash flow.

- You might have to wait 6 months after purchase before refinancing

- You may have to pay financing fees twice (at purchase and at refinance)

For more details in the Big Horn deal, you can also check out the following blog posts:

- Big Horn – Purchase Breakdown

- Full details on how we purchased this property

- Big Horn- Deal or No Deal

This post may contain affiliate links. I may get commissions for purchases made through links in this blog.

Leave a Reply