In my previous post within the Getting Started in Real Estate Series, I discussed traditional or conventional real estate financing strategies. However, what happens when you do not meet the qualifications to get a loan from a traditional lender?

Given that our experience is with rentals, I will stick to buy-and-hold loan products.

First, let’s discuss a few reasons why you would have to use alternative financing methods:

- Your Debt-to-Income ratio is too high. (Refer to Part 1 for a refresher on Debt-to-Income

- Your credit score is not high enough or don’t have enough credit history

- You are borrowing some of the funds for the down-payment

- The house you are buying is in deteriorating condition and not habitable

- You are self-employed and don’t meet the 2-year requirement

Next, let’s talk about possible solutions.

Keep in mind that these alternative products will likely be more expensive than going through the traditional route, so you must keep this in mind as you analyze deals.

Hard Money Loans

Hard money loans are asset-based loans secured by real estate. These loans are typically issued by private equity investors or companies. Hard money lenders are not banks; they are investment companies. They are also not regulated as much as banks which allows them to be more flexible. These loans will likely have additional upfront costs (points) and higher interest than banks would given the higher risk and shorter duration.

In essence, Hard Money loans are also private money loans because the funds are ultimately coming from individual investors. In some cases, private money and hard money loans are used interchangeably. For the purposes of this blog post, I will refer to Hard Money Lenders as companies that have an established lending business and Private Lenders as individuals like you and me that lend money as an additional investment vehicle.

Normally, a hard money lender has predetermined lending products. They are structured and your lending profile will determine the products that you are eligible for.

Examples of hard money lenders that are well-known: Kiavi, LimaOne, LendingOne, Visio Lending, etc.

I will discuss different types of hard money loans below.

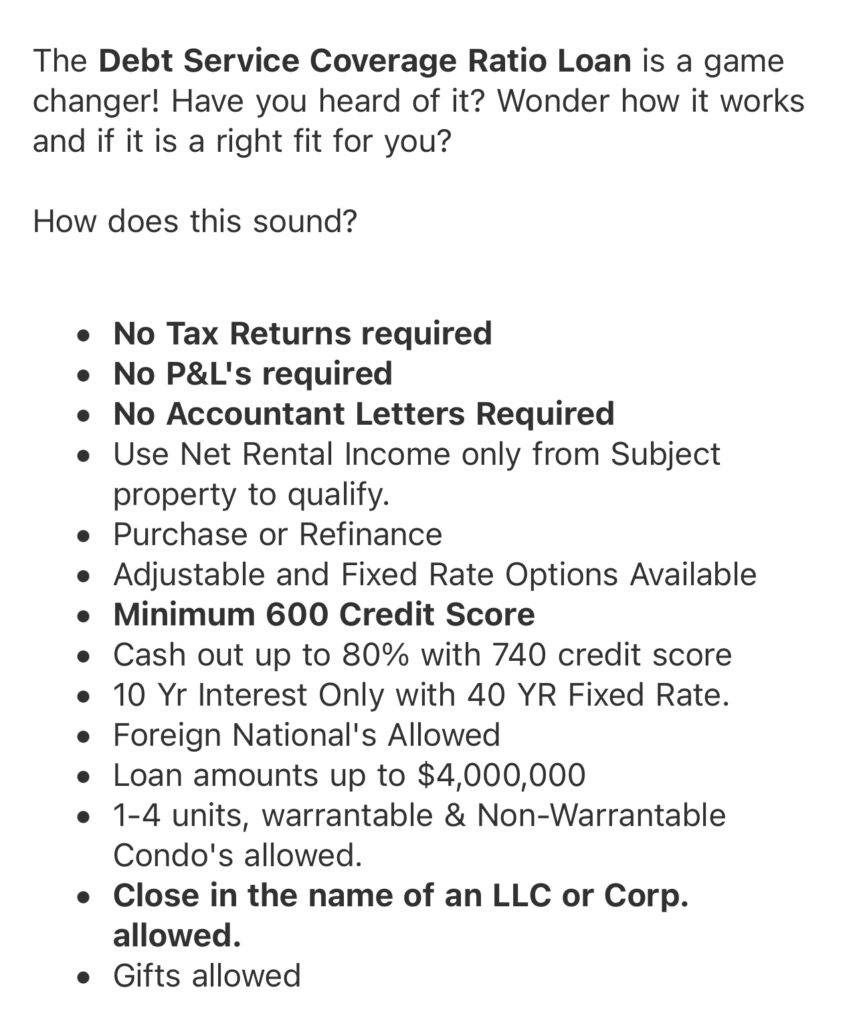

DSCR Loans

These are the no-doc loans we hear about. DSCR loan is a type of hard money loan that is based on the income of the property and not your income as a borrower. Therefore, you won’t have to provide proof of income or tax returns. However, the property’s income will need to be sufficient to cover the debt of the property, operating expenses, and more. These are perfect if you are unable to get traditional lending due to your DTI, insufficient income, or you are self-employed and don’t have 2-years of tax returns.

DSCR loans are typically for properties that are ready for long-term financing. Great for short-term rentals as well.

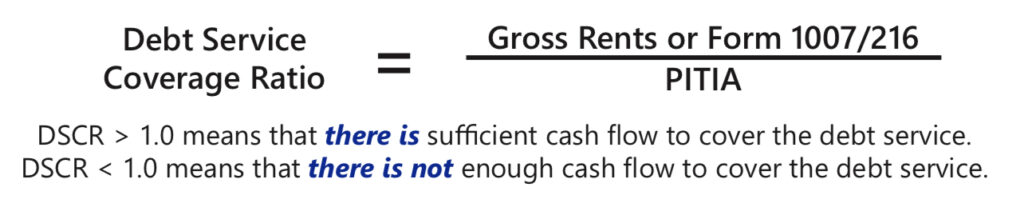

What does DSCR stand for?

Debt Service Coverage Ratio. It is calculated as follows:

The same companies I mentioned above offer DSCR loans: Kiavi, LimaOne, LendingOne, Visio Lending, etc.

In the last year, I have also seen some conventional mortgage companies add DSCR products. For example, Fairway Independence Mortgage was go-to for conventional loans and now they have an investor loan program.

Type of Documentation Required

While they are referred to as “no-doc” loans, there is still some documentation required.

- Company Organizational Documents (Articles of Incorporation, EIN, Operating Agreements):

- In most cases, hard money lenders will require that the property be purchased under a legal entity (though there are exceptions). This could be an LLC or any other legal entity as recommended by your CPA or Attorney.

- Real Estate Owned/Transaction Schedule (REO):

- In the hard money world, the more deals you have under your belt, the lower the risk. The lower the risk, the lower the fees. Your experience comes into play when determining the terms to offer you.

- If you don’t have any deals under your belt, That’s okay. It just means you will be paying interest on the higher end.

- Authorization for Credit Check:

- Your credit score will be factored in the determination of the terms offered. A lower credit score means higher risk, and therefore, higher fees. Depending on the lender, they will have a minimum credit score requirement, but they could be more lenient compared to traditional lenders.

- Most hard money lenders will do soft credit checks which I personally love. These will not affect your credit score.

- Executed contracts

- As with any real estate transaction, you will have to provide an executed purchase contract. If it’s a refinance, then you will provide current mortgage information and a payoff letter.

- Verification of primary residence

- This is not the norm for everyone, but some lenders may require that you own your primary and make you sign an affidavit to make sure that you won’t occupy the property as your primary. Especially in homestead states, this is of great concern to them. We even had to show proof of on-time payments in our primary home as well.

Typical Terms from DSCR Loan

- The terms will vary widely depending on the lender, the property itself, the property income, your experience, and credit. Examples of what I have seen offered are:

- 5/1 ARM which is a 5-year fixed rate and an adjustable rate after that with a 30-year amortization.

- 7/1 ARM which 7-year fixed rate and an adjustable rate after that with a 30-year amortization.

- 30-year fixed rate.

- 40-year amortization, interest-only loan.

- The interest that I have seen is generally 1% -5% higher than other loans. Normally, adjustable loans with a lower fixed rate term will have better rates.

- Origination costs are also higher, typically 2-5% as well.

- We have seen some 15% down DSCR products for short-term rentals recently.

Here is an example of an email I received from a lender offering DSCR products.

Case in point

Our first investment property was purchased with a hard money lender called Velocity Mortgage. We went through a broker that found the best hard money lender for our specific needs at the time. Our properties were two duplexes with tenants in place. We didn’t want a bridge loan (discussed below) because we weren’t sure that we would complete the repairs within 12 months, so we went with a DSCR loan, a 30-year fixed amortizable loan.

The key item was that we needed a lender that did not require proof of funds or seasoning of the funds because we were going to borrow the entire down payment.

It was the first investment property, so we had to provide LLC docs, Ryan’s credit report, and sign a certification that we would not reside in the property and proof that we had made timely payments to our primary mortgage in the preceding 12 months.

Then, we got two personal loans for the down payment. Now, this is not something I would recommend to a beginning investor. This was a very bold move, and you can read all about this here. If you are going to borrow 100% of a deal and use a combination of loans, you need to have your personal finances organized. You need to really understand your numbers and have a plan on how you will pay those loans in the event that things don’t go according to plan. In our case, we had a budget, and backup loans and we had monthly income after our expenses left to pay for these loans without counting on the property income, but we were tight.

Fix-and-Hold and Bridge Loans for Rentals

When a property needs full rehab and doesn’t qualify for traditional financing immediately, you may need to use a fix-and-flip type product. Generally called Bridge Loans. As the name implies, these are loans that will help bridge the gap while you rehab the property and secure conventional financing. Normally, these loans have higher interest rates, for a period of 12 to 18 months and no prepayment penalty. You should also expect to pay a few points upfront (2-3%) plus underwriting and/or admin fees.

The goal when getting a bridge loan is to complete the rehab and secure long-term funding as soon as possible.

Some of the larger hard money companies like the ones mentioned previously provide a bridge loan that can or will be converted to a long-term rental loan as soon as the rehab is completed.

In the fix-and-hold scenario, you can either get financing for a percentage of the purchase price or a percentage of the after-repair value including repairs. If you have a really good deal, a strong borrower profile, and a flexible lender, you may be able to acquire the property at 100% of the purchase price.

However, most lenders have a max on the loan-to-cost value because they want you to have some skin in the game.

Case in point

Let’s say you have a property with the following facts:

- Purchase price (Cost) of $100,000 with

- After Repair Value (ARV) of $200,000

- Rehab cost of $60,000

The hard money lender may offer 80% of ARV (or $160,000), limited to 90% of Loan-to-Cost ($90,000). This means that you will have to put 10% (or $10,000) down. Creative financing tip: This down payment (if supported by the numbers) may possibly be another loan from private money, lines of credit, etc.

For a deal like this, they can add a construction loan-type product where you can draw to complete the rehab. In a lot of cases, I have seen that they will do either 90% or 100% of the rehab cost which is not bad at all.

Note that most of these construction loan products require you to upfront the cost and once proof of completion and receipts is submitted, they will send you money in draws. Yes, there are some exceptions, but the majority of quotes I have gotten work this way. Additionally, depending on the lender, a third-party inspection may be required prior to getting reimbursed. Furthermore, there might be fees associated with each draw (between $150-$300). These are important considerations of going with a rehab loan. Creative financing tip: This is where a private money loan, line of credit, credit card, or personal loan may come in handy as well.

If the numbers for the above deal were also really good, I would probably get the $90,000 loan with a $60,000 rehab loan plus $30,000 of lines of credit. I would use $10,000 for the down payment, then $20,000 to use to front the construction costs.

If you are going to use borrowed funds for down payments, always make sure that your lender doesn’t require seasoning of the funds. Seasoning means that you have to show proof that those funds have been in your account for 60-90 days (depending on the company).

Wrapping it Up.

Hard money lenders are a great tool to have in your toolbox. They have evolved over time. Some people think of hard money lenders as the sketchy old man with money, but nowadays, with all the private equity funds needing to put their investor’s money to work, we have so many options available to us from reputable companies. Now, that’s not to say that there aren’t any sketchy companies out there. You still want to vet them out.

I wanted to go into as much detail as possible, so this section ended up being a bit longer than anticipated. I hope you find this helpful.

I will have an additional post that will focus only on Private Money Loans and how to structure these.

See you soon! Don’t forget to subscribe so that you can be the first to know when new posts go live!

This post may contain affiliate links. I may get commissions for purchases made through links in this blog.

Leave a Reply