So you are making more money than you spend. You have extra cash available each month, what then?

When it comes to extra cash, I know three types of people:

A) The ones who can’t have cash and will spend it all. The moment they have extra cash, they go on a shopping spree.

B) The ones who like to hold on to cash like Gollum from Lord of the Rings held on to his precious ring. The extra cash sits in a savings account either getting 0% or very low interest.

C) And finally, the ones that put every dollar to work into high yield investments like index funds or real estate.

Sadly, a lot of the people I know fall into group A. I, too, was part of this group not too long ago.

More often than not, group A individuals just don’t know what to do with their money. They don’t teach us personal finance in school, so most people don’t know how to enter the group C club. Some don’t even know that there are ways to make their money work for them. Therefore, they spend their money on buying the things we are told matter: the nice house, the nice house, the nice shoes, etc.

Now, group B individuals are interesting because they are quite responsible with their money, they’ve worked hard to save up and are afraid to lose it. They call this a scarcity mindset. Individuals in this bucket are afraid that money will stop coming and therefore need to cling to their money. Having the cash gives them a sense of security.

This is quite the predicament because while the stock market has its ups and downs, it has proven to build wealth over time rather than decrease it.

Of course, not everyone in this bucket is that extreme, but I do know of people who hold large amounts of cash “just in case” and it pains me.

Finally, let’s talk about type C individuals. I just made it to this bucket not too long ago so I don’t have a whole of experience. What I do know is that those on the path to wealth do not hold on to their cash.

I have many years of experience recklessly spending money though and I know that having cash in the bank is dangerous for me. It’s an unnecessary temptation, so I put every possible dollar to work ASAP.

I recently read online that you should look at your money like little workers. Would you hire workers to sit at home or would you put them to work? I probably butchered this analogy, but hopefully you got it!

So what to do with your extra cash? Invest it! Here are three ways that I invest my excess after-tax cash on a monthly basis.

Note that I am emphasized after-tax. If your company offers deferred tax retirement accounts like 401k or 403b, you might want to contribute to those plans first. If your company matches any of your contributions, you should at least contribute enough so that you can get 100% of the company’s match. That’s free money.

Now, back to after-tax options…

Roth IRA

If your adjusted gross income is less than $139,000 (if single) or $206,000 (if married), opening an IRA could be a good way to invest your excess money. The reason I point out the income limits is that the IRS won’t let you put money in a Roth IRA once you exceed this income limit. At this point, the IRS says that you make too much money to be eligible.

What is a Roth IRA?

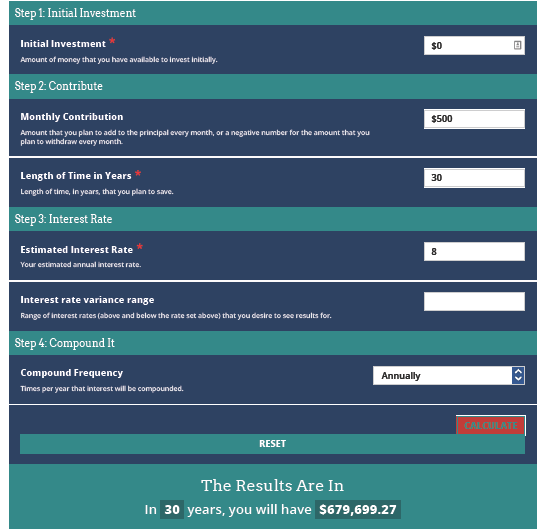

A Roth IRA is a special type of retirement account that allows you to put your after-tax dollars (your take-home money) to work and all earnings from this account are tax-free as long as you don’t withdraw the gain portion from these investments before age 59 1/2. The IRS allows you to make an annual contribution of up to $6,000 a year or $500 per month.

Let’s assume you have 30 years until you turn 59 1/2. If you were to put $6,000 a year (total $180,000 over 30 years) it would be worth about $680,000 by the end of the 30 years. The gain would be $500,000. At a 20% capital gain tax rate, that would be $100,000 in taxes, but because the Roth IRA earnings are not taxable, you won’t have to worry about paying taxes when you start withdrawing your Roth IRA money.

Another big perk of Roth IRAs is that you can withdraw your contributions at any given time without a penalty. This is not something you can do with any of the other retirement account options out there.

If you want to play with the calculator shown above, go to investor.gov here

Where and how can you open a Roth IRA?

Pretty much every brokerage, bank, or investment company has options to open a Roth IRA. This is something you can do yourself from home. Most services are very user-friendly and you can open an account within minutes. Here are 5 companies that you can use to open a Roth IRA

- Vanguard: Link to site here

- Fidelity: Link to site here

- TD Ameritrade: Link to site here

- Wealthfront.com: Link to site here (FYI this is an affiliate link)

- Sofi.com: Link to site here (FYI this is an affiliate link. You get a $50 bonus if you sign up with this code)

There is an infinite list of options out there. Do your research. Don’t just take my word for it. Each website has resources available that give really detailed explanations on their retirement accounts. The general concept and benefits of the Roth IRA will be the same from company to company. The difference is the platform (user-friendliness and reputation) and the types of investments you can select.

Low-Cost Index Fund or ETFs

After you have taken advantage of tax-favored portfolio investments, you could invest in the stock market through index funds or ETFs.

Index funds and ETFs are both a pool of stocks and bonds mixed together into one single share. For example, an ETF or index fund based on the S&P 500 bundles up shares of the top 500 companies in the country. These companies include Apple, Amazon, etc. When you buy a share of an S&P 500 ETF, you are buying a small amount of shares of those 500 companies included in the bundle. This makes the investment less risky because the chances of all 500 companies going out of business are very unlikely and these companies are within multiple industries.

ETFs and index funds are pretty similar in nature. Explaining the differences between the two should be its own post, but the main difference between ETFs and index funds is that you could trade ETFs during the day whereas Index funds will be traded at the end of the day. The value of shares will vary throughout the day and if you invest in an ETF, you could potentially buy at midday when the prices go down. The value of index funds doesn’t get updated until the end of the day.

At the end of the day, you can’t go wrong with either of the two options. Personally, I invest in Vanguard Total Stock Market Index Fund Admiral Shares (VTSAX) using Vanguard.com. After reading The Path to Wealth by JL Collins, I decided that was going to be my primary go-to index fund. You can check out the book on Amazon here.

Personally, I have a weekly auto-purchase going into my Vanguard.com account. This is part of my required monthly contributions in my budget and any extra cash at the end of the month will be allocated between our various investment accounts.

Auto-transfers are not possible with ETFs which is why I prefer index funds.

Where and how can you start investing in index funds or ETFs?

Index funds and ETFs are bought through brokerage accounts. Any of the options I provided for the Roth IRA above will work, but here are a couple of additional options:

- Acorns: Link to site here. They require you to pay a $1 per month subscription fee which I don’t love, but they do have the round-up option where they will invest your change for every purchase you make. This is good for those that say “I have no money to invest”

- Robinhood: Link to site here. If you use my link, we both get 3 free stocks. I have a few hundred dollars in that account. Mostly money I got for free, but Robinhood is very user-friendly and they even have crypto options if that’s your kind of thing.

- Personal Capital: Link to site here. If you use my link, we both get $20. I don’t have much here, but I do use Personal Capital for my Net Worth tracking. I like their performance analysis option.

I prefer to keep everything in one place so my main account is at Vanguard. I do like having surprise money that I can cash out whenever I want to splurge. These other small amounts I keep for a rainy day.

Real Estate

Of course, Real Estate is in my top three ways to invest your extra money. Because, why not?!

I left it for last because buying real estate property is not as accessible as the above two options, but it is my favorite and where most of my money goes.

I genuinely think real estate is a great way to set yourself up financially. Not just because of the income, but also because of tax advantages. I am not going to go into detail in this post, but one of the reasons is due to a tax write-off called depreciation. I am linking a more detailed article here for you to read more on this. Basically, the IRS says that when you buy a property, it will lose taxable value each year. Depending on whether you have a residential or commercial investment, the expected life of a property is either 27.5 or 39 years. This means that by year 27.5, your single-family rental will be worth $0 according to the IRS. I love this deduction, but let’s be honest, this does not reflect the reality. As long as you keep the property long-term, you will enjoy this write-off. A lot of properties end up having “paper losses” because of depreciation and not pay taxes on any of the profits. This is because the rent income you earn is less than your monthly expenses (mortgage interest, taxes, maintenance, etc.) plus depreciation expense.

However, that is not the reason I invest in real estate. For me, it’s all about the cash flow. Consistent monthly income. This is key for our early retirement plan.

How Do I Start Investing?

I understand that buying real estate is not as easy as buying stocks and I have several blogs in the Real Estate Investing category where I discuss how to get started and provide you with details of how we got started without having money.

My take on real estate investing is that you don’t need a lot of money to get started if you get creative. However, you will have to have some money. If you have gotten this far in this blog post, I assume you have some extra money that you can invest.

This is a big topic, so I am working on providing a more detailed step-by-step blog on how to get started, but here is a quick run-down assuming we are going the conventional route.

- Know your credit: Your credit score will determine what route you will need to take. You may need to get your credit situation sorted out before you get started and this can take some time. It is not impossible to get started with bad credit, but it will require creativity.

- Do some studying: While real estate doesn’t have to be complicated, there are a few things you want to know before you get started. We don’t want you to start completely blind. Reading my blog, listening to podcasts for example. All of BiggerPockets books, blogs, podcasts and forums are great sources for real estate education.

- Explore your options: Go to Zillow, Realtor.com, Redfin. You can start with a Google search for Real Estate for sale near XYZ city. I recommend that you have an idea of what is out there before speaking to a realtor. Realtors are great to help you get to the finish line, but if you don’t know what you want, it is going to be really hard to communicate with a realtor. You also want to have realistic expectations. You can’t ask your realtor for a $10,000 house in Miami. Not happening.

- Find a Lender: If you are going to be using any type of financing, you would need to find a lender first and get pre-qualified. Realtors will not do showings without a pre-approval.

- Find a Realtor: Get referrals from your network. Preferably work with someone that also invests in real estate or at least understands how investment transactions work.

- Focus: Once you have spoken to a realtor and gotten access to the listings, figure out what type of investment you want. You want to narrow down your search as much as possible. I want single-family home in the $100,000-200,000 that rents for $1,000-2,000 per month in these zip codes.

Alternative Real Estate Investing Strategies

By now you must be tired of reading, but I didn’t wanted to add that buying a property is not the only way to invest in real estate.

You could buy Real Estate Index Funds using the options provided in either 1 or 2 above.

There are also crowdfunding companies like Fundrise (link). I don’t currently own any investments in any of these because I prefer to buy the actual property myself, but I would otherwise.

Real estate loan investing is another option. There are several options out there. I have about $300 invested in Ground Floor. I wanted to try it out before I put in a significant amount of money. So far, I made about $18 dollars! Interest on the loans I invested was 10% and 14%. Not bad, right? The loans get repaid every 6-12 months depending on your selection.

As I write this, I realized that Groudfloor.us now has a self-directed IRA option, so you can take advantage of tax deferral and also invest in real estate loans. If you are interested and use my referral link, we both get $20.00. Referral here and info to self-directed IRA is here. Note that self-directed IRAs have more rules than a traditional IRAs or ROTH IRA. Make sure to do some reading.

I will be writing a more detailed post on these alternative real estate investment options later on. Stay tuned!

This post may contain affiliate links. I may get commissions for purchases made through links in this blog.

Leave a Reply