Buying property cash may or may not make sense in certain situations. If you ask Dave Ramsey, the answer is yes, but if you ask me, the answer is… Depends.

If you have read any of my real estate investing blog posts, you know I am a big fan of using debt to buy real estate investments. However, this is because of my circumstances and goals.

When it comes to personal finances, everyone’s journey is different. I can only provide insights into why I do what I do and my perspective on buying rental properties cash.

In this blog post, I am going to walk you through an example scenario that illustrates why I prefer to have a mortgage rather than buying rental property cash.

Why I don’t buy investment properties with my own cash

Note that I am emphasizing “my own money”. The truth is that I don’t have cash of my own. At the time of this post, I am in the baby phase of my real estate investing business and I still working out my personal finance situation.

Assuming that I did have cash available, would I then buy an investment property cash? Yes, but I would most likely turn around and get a mortgage.

This is actually what we do. We buy properties in cash (not our own) to secure more advantageous pricing and then turn around and get a mortgage after the purchase. Purchase-> Finance. If you want to learn more about how we do this, be sure to check out our Here is the Deal Series of posts. In these posts, I walk you through how I do this.

My hubby and I are working towards building a solid real estate portfolio that will provide an income sufficient to cover our living expenses. Buying real estate using debt allows you to grow a portfolio faster. This is the #1 reason that I prefer to use debt rather than locking down my available cash.

What if growing a portfolio is not your goal? Is buying a property cash a good idea then?

Not everyone wants to have multiple investment properties.

I know plenty of people who just want one rental paid off and provide supplementary income. Your goal might just be to diversify your investments and sources of income.

In this case, would it make sense to buy cash? Depends.

Ask yourself, is there a better use of the cash you would have otherwise borrowed?

Mortgage rates are usually lower than many investment returns. What if you could invest the money you borrowed into an investment vehicle that gives you 6% returns and your mortgage interest rate is 4%? Wouldn’t that be a better option?

Let’s test this out together:

I am going to use a very simple scenario and use a few online calculators to better illustrate the example.

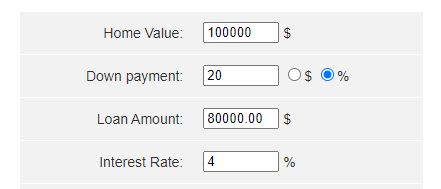

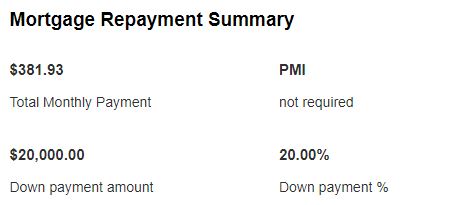

Let’s say you had $100,000 cash and there was a rental property available for purchase for $100,000

Property Details

| Monthly Rent | $1,000 |

| Monthly Taxes and Insurance | ($200) |

| Monthly Reserves for Vacancies, Repairs & Improvements | ($200) |

| Property Cash Flow (No Mortgage) – Scenario 1 | $6000 |

| Mortgage Payment @4% interest (rounded) | ($400) |

| Property Cash Flow (with Mortgage)- Scenario 2 | $200 |

| Cash needed for purchase (no mortgage) – Scenario 1 | $100,000 |

| Cash needed for purchase (mortgage plus loan costs) – Scenario 2 | $23,000 |

I used www.mortgagecalculator.org to calculate the mortgage payment as shown below.

A couple of things to note. Rent prices will go up over time, but this doesn’t impact the example above because we assume that you would be contributing the net property cash flow in both scenarios.

Next, let’s look at the hypothetical investing scenarios.

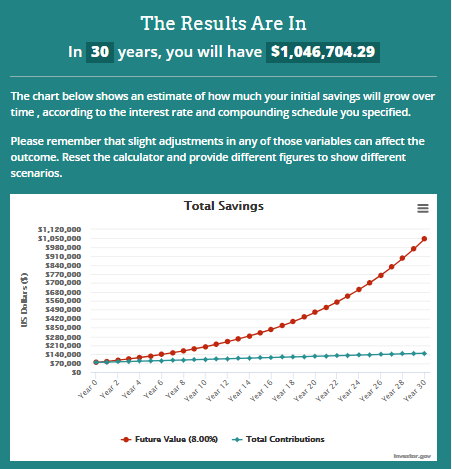

Scenario 1

Use $100,000 to buy the property cash and invest the $600 monthly cash flow into an index fund like the S&P 500 earning an 8% annual return.

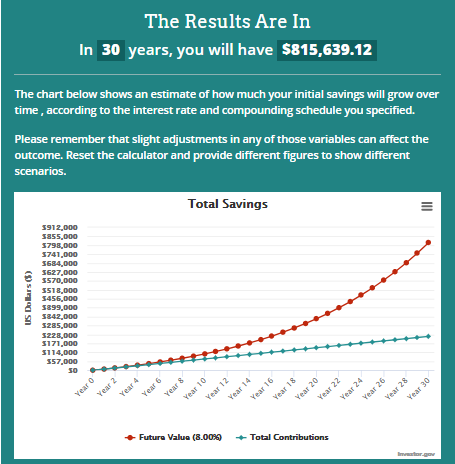

Scenario 2

Use $23,000 for a down payment and invest the remaining $77,000 plus the $200 monthly cash flow into the same index fund portfolio earning an 8% annual return.

Note that research has shown that the average annualized return for the S&P 500 has been 10%, but let’s just be a bit more conservative.

I used the calculator in investor.gov for the calculations below. Click here to do your own calculations.

Which scenario is best?

There is no right or wrong answer to whether buying a property cash or financing it is a good idea. There are various reasons why financing a property may not make sense or is not even possible.

- The property may not cash flow much if you had a mortgage, or perhaps you don’t qualify for a mortgage.

- You don’t qualify for a loan

- Perhaps you don’t like the volatility of the stock market. My dad, for example, will not invest in the stock market even if I paid him to.

Please keep in mind that the above scenarios were simplified for illustration purposes. I just wanted to present a scenario where you can mix and match to maximize your returns. As you can see, scenario no. 1 will yield the highest return after 30 years.

Quick Note

In both scenarios, the property value will be the same. The purchase price is the same whether you buy cash or finance.

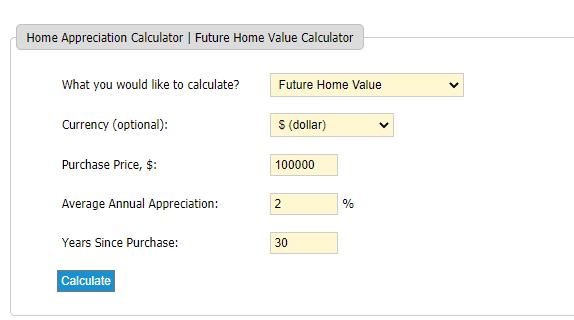

I used an online home appreciation calculator to help me with this example.

At a 2% house value appreciation rate, the property value will be $181,000 in 30 years.

To try it out yourself, click here

Wrapping It Up

Buying a property cash is not always a bad idea. Using debt is not a bad idea either. It all depends on your goals and circumstances.

Thanks for reading!

If you liked my content, don’t forget to press like below. It means the world to me!

This post may contain affiliate links. I may get commissions for purchases made through links in this blog.

Leave a Reply